The hardest problem I worked on at DAT

Ownership Before Form Factor

John Leo Szrejter · Perspective

How I reasoned about the next generation of American road freight matching, and why the obvious move (build the unifying product first) is the wrong place to start.

Everyone in American road freight is jumping between five systems to move a single load. Shippers, brokers, and carriers all burn time stitching together tools that were never built to talk to each other. The obvious fix is to build the one platform that finally unifies them.

That instinct, build the unifying product, is where most platform strategy starts. It is also where most of it goes wrong, because it treats form factor as the first decision. Form factor is the last decision.

Here is the thesis: what you can own determines what form factor can win. Before you design anything, you map who already owns each high-trust decision point across the freight journey, then decide what to own, what to partner for, and what to buy. The product that wins is the one your ownership position actually lets you build. Maturity, meaning how far you can reliably push automation at a given point, gates the rest. Start with the product you wish you had and you will design something your ownership position cannot support.

Where I was sitting

I led research for DAT One, the load board behind 65 to 70 percent of the U.S. spot freight market, a $350 to $400 million annual-revenue product running near 40 percent EBITDA with ties reaching into contract freight. I owned its research landscape and was tasked with identifying the strategy for the next generation of American road freight using everything we had: an internal research team, a $5 million Roper-funded research engagement with Bain, and more first-party freight data than anyone else in the market.

None of that was required to see the environment was fragmented. It was required to decide what to do about it.

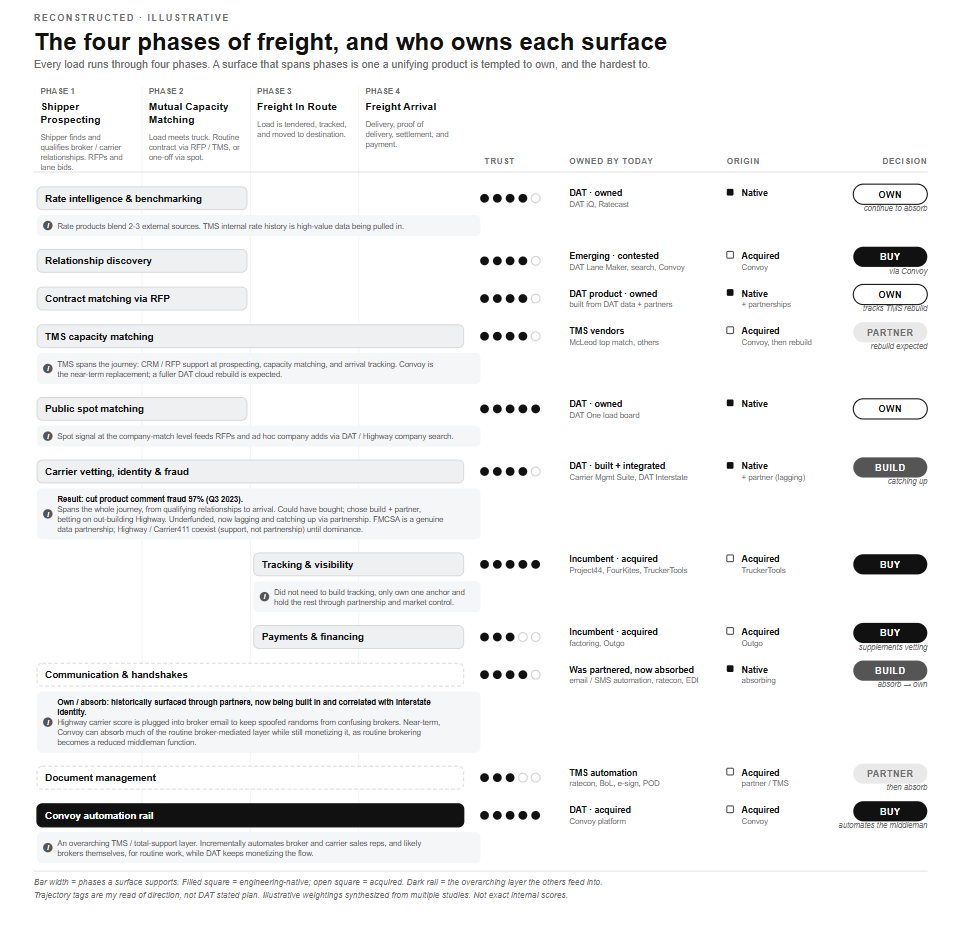

The method: map who owns each trust point

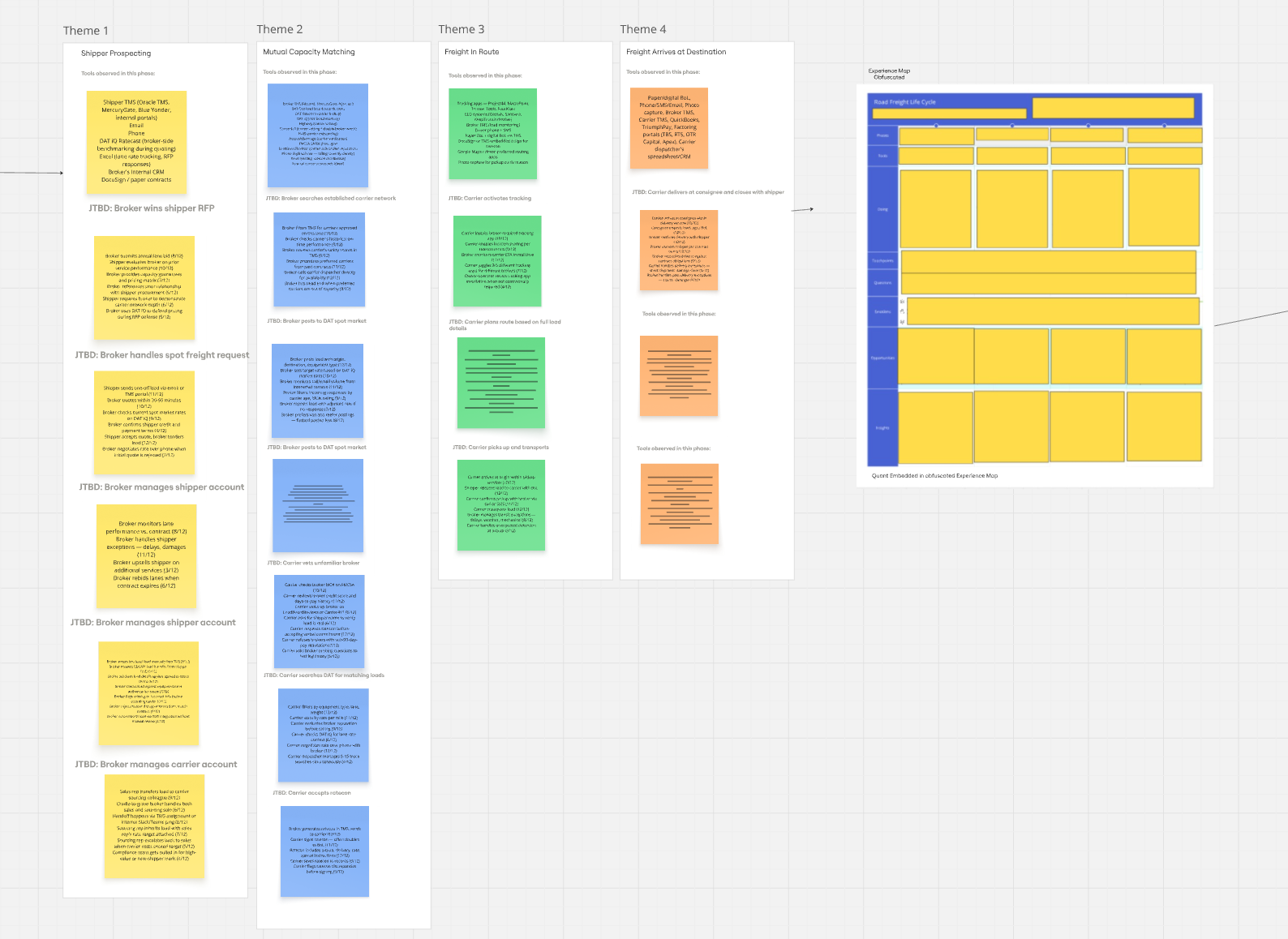

I built an end-to-end experience map of the entire freight journey: Shipper Prospecting, Mutual Capacity Matching, Freight In Route, and Freight Arrival at Destination. At every stage I mapped what we owned and led, what we did not, who the personas were, who the incumbent leaders were, the current quality of the experience, and how hard it would be to move a user from one product to the next. My product partners mapped the other half of the board: each leader's market penetration, the difficulty of transitions between products, and the profit-to-team-cost ratio of each play.

The decision points are not equal. Some carry far more trust weight than others, which means whoever owns that point sets the standard everyone downstream has to follow. Tracking is the clearest example. The party who chooses the tracking tool effectively decides it for the others. Mapping where trust concentrates is what tells you which points are worth owning and which you can safely partner around.

From map to ownership strategy

The question every C-suite asks in a blue-sky landscape is "do we build or buy this?" The real answer in freight is usually "partner, until you can't." You partner until the friction of depending on someone else outweighs the cost of owning it. Transition abrasiveness, meaning how painful it is to move users or data across a seam, is what usually triggers the first serious build-or-buy argument. Once you decide to own, market penetration, product health, and EBITDA over time tell you which company to buy rather than build. And if your long game is training AI, you want to own the surfaces you intend to train on, because you cannot reliably mature automation on a surface you do not control.

Triangulation

Three signals fed the map: my internal research, the $5 million Roper-funded Bain engagement, and my own field signal. I weighted them by confidence, not by cost. My internal work carried the highest internal and external validity because our research rigor had outrun previous teams'. The Bain engagement was expensive but came with a catch: Roper funded it without buying rights to the underlying data, so we could not inspect how the vendor ran its research or fully audit its findings. Historical research and vendor findings were treated as low-to-medium confidence and directionally useful. My recommendations were treated as medium-to-high confidence and usually adopted as the default read. Where we owned the surface, I used internal qualitative and quantitative signal reduced to high, medium, or low confidence. Where we did not, I filled the gap with work-shadow observation, interviews, surveys, and public competitive analysis.

The TruckerTools decision

This is how the framework picks a path.

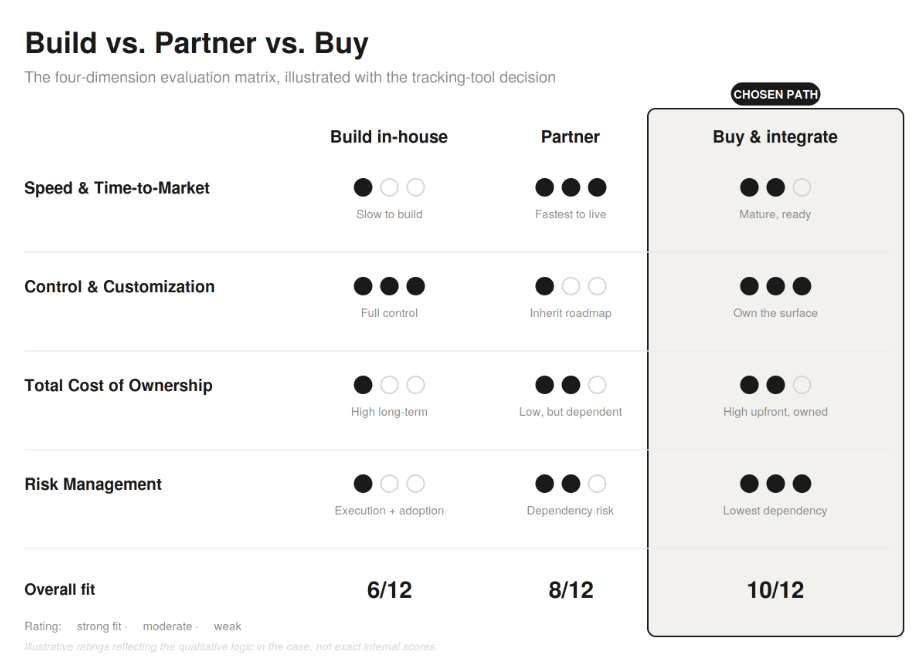

My research informed deprioritizing DAT's own tracking software in 2023 and set up the acquisition of TruckerTools. Three factors drove it. First, across studies with shippers, brokers, and carriers, shippers had the loudest voice in choosing the tracking tool and brokers had the second; tracking was a high-trust point owned from the top down, not something we could win by building a better in-house feature. Second, TruckerTools already had a robust tracking product, deep adoption across other product lines, and a large carrier base with contract-freight ties that DAT lacked. Third, our cloud did not need to house tracking itself. It could integrate with it, which made partnering or acquiring clean from a technical-dependency standpoint. A high-trust point we did not own, an incumbent who already owned it well, and a low integration cost. Buy, do not build.

I ran every build-or-buy call through the same reusable template: four dimensions, scored per option, on a common scale. Run the tracking decision through it and Buy carries the board, not just the conversation.

TruckerTools was the first node DAT chose to own on this logic, and the same template shaped what came next.

From raw research to the map

Competitive wargaming

With the map and matrices built, I ran the right-to-win exercise with product and C-level leadership. We started from the experience map, the matrices, and the user flows, walked them together, wrote out the highest-confidence scenarios, and attacked each one for weakness until a single scenario held up.

To grade each build-or-buy scenario consistently, we scored it against a four-dimension evaluation matrix:

Speed and time-to-market. How fast the play could realistically reach customers.

Control and customization. How much we could shape the surface to our needs versus inheriting someone else's roadmap.

Total cost of ownership. The full cost over time, not just the acquisition or build price.

Risk management. Technical, market, and dependency risk across the life of the decision.

The framework was bottom-up before it was top-down. Historical learnings and field signal funneled into it first; UXR and product started the matrix and populated it with evidence, and executive leadership then led the scoring and final call. That sequence mattered: the people closest to the workflow built the case, and the people accountable for the bet made the decision on a common scale rather than on instinct.

From there we listed the jobs to be done, what an MVP had to have, and the nice-to-haves we already knew about. That package went to C-level for prioritization: each leader scored every effort one to five, and the ranked output came back to us for planning.

Sizing the market, by broker segment

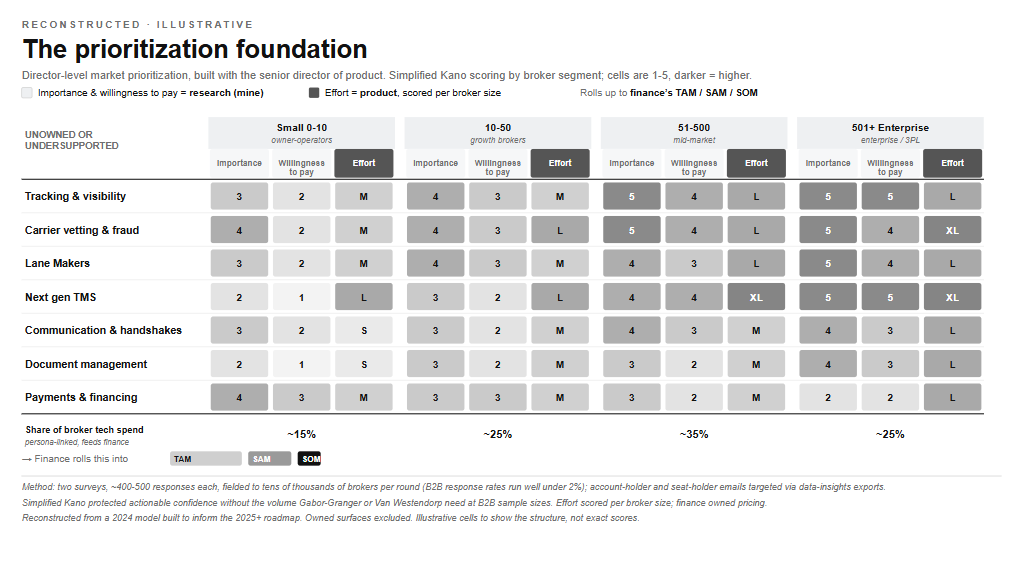

Before any of this resolved into a specific build or buy, there was a prior question: which market do we aim at, and how hard. I built the answer with the senior director of product, as a director-level market-prioritization tool, not an IC-level feature spec.

The evidence base was two surveys, roughly 400 to 500 responses each. Getting there meant fielding to tens of thousands of brokers per round, because broker response rates are punishing, well under two percent in practice. That funnel is the whole reason the rest of the design looks the way it does. At that yield you cannot afford a method that needs heavy per-respondent volume, so I ran a simplified Kano scoring, which protects actionable confidence without the sample sizes a Gabor-Granger or Van Westendorp quietly requires, methods that get statistically thin fast in B2B. Keeping it coarser was also deliberate on the handoff: finance owned pricing, and a simpler instrument let them run with it without a research bottleneck. To keep the sample trustworthy, I set recruitment criteria from our broker personas, then used SQL to export broker lists to xlsx, loaded them into Google Sheets, and targeted account-holder and seat-holder brokers by company size over email through SurveyMonkey. That way the responses came from a healthy ratio of buyers and daily users, not whoever happened to reply.

The structure followed from there. I scored the surfaces we did not yet own or under-supported, segmented by broker size, because we had boiled our personas into population bands (0 to 10, 10 to 50, 51 to 500, 501 plus). For each segment I captured self-stated importance and willingness to pay. Product scored effort per segment, since each size needs a different solution. Finance took the segment tech spend and rolled the whole thing into TAM, SAM, and SOM.

Here is the part that matters, and the part a survey like this cannot do. It captures how the market sees and ranks today. Respondents can rank the needs they already understand. They cannot see the future state we have in progress; they cannot price the surfaces we need to own to build and scale AI, and they cannot gauge a maturity that only reveals itself as you ship. That understanding scales over time, through incremental product development, not through a one-time survey. Treating a desirability scan as a roadmap is how teams build the wrong thing with confidence.

So this artifact does one job, and only that job: it points the strategy at which markets to prioritize and roughly how, plus the high-level needs inside each. What to actually build inside that market is a separate, downstream question that lives in PRDs and the product cycle. This is the foundation, not the floor plan.

From there it became a living input, not a one-time deliverable. It informed the ongoing build, buy, and partner work directly: we shipped first iterations of the surfaces it prioritized and kept maturing them as the bigger ownership calls got made around them. The clearest example of one of those calls, and the first major acquisition it helped tee up, was tracking. That is the TruckerTools decision.

What this transfers to

The freight specifics matter less than the sequence, and the sequence travels to any fragmented platform landscape:

Map the end-to-end experience.

Find the high-trust decision points and ask who owns them.

Partner until the seams hurt, then let penetration, product health, and margin pick your buy target.

Own the surfaces you intend to train automation on.

Decide form factor last, because what you can own is what you can build.

Where this is heading

The goal is to turn a load board into the operating system for American road freight, and it is happening in public. A traditional load board is a posting site: matches happen on the platform, but the deal, the payment, and the execution happen somewhere else. The next generation closes that loop and runs the whole transaction on one surface.

DAT has been assembling that surface node by node along the pipeline. It acquired TruckerTools for visibility and tracking, Outgo for payments and financing, and the Convoy platform for end-to-end capacity matching and execution, while phasing out its older TMS. Each one is a high-trust decision point the company chose to own rather than depend on, and each is integration-viable rather than a ground-up rebuild. That is the build/partner/buy framework running at company scale: own the surfaces that anchor trust and that you intend to automate on, integrate where you can, and consolidate the pipeline into a single operating layer.

The scale signals the stakes. As FreightWaves has reported, DAT's parent Roper carries roughly a $60 billion market cap and has put over $450 million into freight-tech acquisitions in a span of months, with the Convoy platform reported around $250 million. These are large bets on owning the matching layer outright, and they follow the same logic the experience map surfaced: the company that holds the end-to-end ownership position is the one that gets to define the form factor everyone else has to plug into.

Example in house build recommendation shipped : see the DAT Carrier Management Suite case study.

References and sourcing

The acquisition sequence (the nodes) DAT acquires Trucker Tools (closed December 17, 2024). DAT release: https://www.dat.com/company/news-events/news-releases/dat-acquires-trucker-tools-an-innovator-in-real-time-load-tracking-and-visibility and FreightWaves: https://www.freightwaves.com/news/dat-acquires-trucker-tools-leadership-speaks-on-tech-goals-for-2025

DAT acquires Outgo (announced May 15, 2025). Press release (Nasdaq/BusinessWire): https://www.nasdaq.com/press-release/dat-redefines-freight-payments-outgo-acquisition-2025-05-15 and FreightWaves, "DAT acquires Outgo, enters race to become dominant freight exchange platform": https://www.freightwaves.com/news/dat-acquires-outgo-enters-race-to-become-dominant-freight-exchange-platform

DAT acquires the Convoy platform (July 2025, reported around $250M). FreightWaves, "Load-matching wars escalate as DAT snaps up Convoy": https://www.freightwaves.com/news/load-matching-wars-escalate-as-dat-snaps-up-convoy

DAT corporate profile (the stack, in DAT's own words). https://www.dat.com/

"Roper Builds All-in-One Freight Platform Around DAT Ecosystem," Supplychain360 (July 2025).https://supplychain360.io/roper-builds-all-in-one-freight-platform-around-dat-ecosystem/